New Delhi : For decades, the National Capital Region (NCR) housing market was largely shaped by regional developers with deep local expertise and established land banks. Today, this scenario is seeing notable transformation. National developers who previously focused mostly on their home markets like Mumbai, Bengaluru, Pune, Hyderabad, and Ahmedabad, are steadily expanding into NCR – highlighting a broader shift towards a more institutionalized and brand-driven residential real estate landscape.

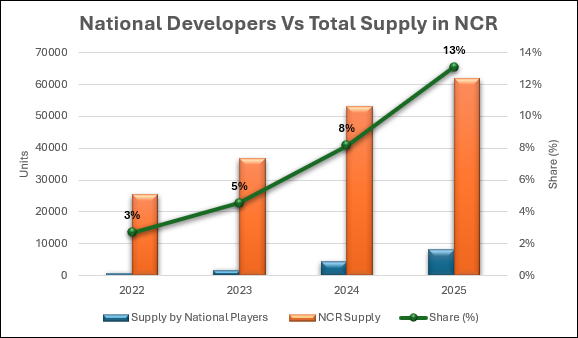

According to latest ANAROCK Research data, the share of new NCR residential supply by national developers has quadrupled in the last four years – from 3% of the region’s total new residential supply in 2022 to over 13% by 2025-end. These players include Godrej Properties Ltd., Prestige Estates, TATA Housing, Mahindra Lifespaces, Adani Realty, Sobha Ltd, Shapoorji Pallonji Group, and Birla Estates.

Regional players continue to dominate this market, but large and listed developers from beyond NCR are now actively participating in its ongoing housing market evolution.

Santhosh Kumar, Vice Chairman – ANAROCK Group, says – “Of approx. 25,355 residential units launched in NCR in 2022, national developers spoke for just 3%, or less than 700 units. In 2025, out of the approx. 61,775 units launched in the entire region, nearly 8,100 units were by national players. Their participation reflects this markets’ increasing institutionalisation, as well as homebuyers’ growing preference for trusted brands with strong execution capabilities.”

New Delhi, 23 June 2026: For decades, the National Capital Region (NCR) housing market was largely shaped by regional developers with deep local expertise and established land banks. Today, this scenario is seeing notable transformation. National developers who previously focused mostly on their home markets like Mumbai, Bengaluru, Pune, Hyderabad, and Ahmedabad, are steadily expanding into NCR – highlighting a broader shift towards a more institutionalized and brand-driven residential real estate landscape.

According to latest ANAROCK Research data, the share of new NCR residential supply by national developers has quadrupled in the last four years – from 3% of the region’s total new residential supply in 2022 to over 13% by 2025-end. These players include Godrej Properties Ltd., Prestige Estates, TATA Housing, Mahindra Lifespaces, Adani Realty, Sobha Ltd, Shapoorji Pallonji Group, and Birla Estates.

Regional players continue to dominate this market, but large and listed developers from beyond NCR are now actively participating in its ongoing housing market evolution.

Santhosh Kumar, Vice Chairman – ANAROCK Group, says – “Of approx. 25,355 residential units launched in NCR in 2022, national developers spoke for just 3%, or less than 700 units. In 2025, out of the approx. 61,775 units launched in the entire region, nearly 8,100 units were by national players. Their participation reflects this markets’ increasing institutionalisation, as well as homebuyers’ growing preference for trusted brands with strong execution capabilities.”

It also highlights the growing confidence of India’s most prominent real estate brands in their ability to expand beyond their traditional home markets and tap into the opportunities of one of the country’s largest residential markets.

It also highlights the growing confidence of India’s most prominent real estate brands in their ability to expand beyond their traditional home markets and tap into the opportunities of one of the country’s largest residential markets.

Supply Dynamics

Collectively, these national players launched over 15,130 units across 30 residential projects in Delhi-NCR between 2022 and Q1 2026. Among them, Godrej Properties has emerged as the most active – by a significant margin. It accounts for over 47% share of the total units launched by the analysed developers, establishing a strong presence across Gurugram, Noida and Greater Noida. Godrej’s strategy of entering multiple micro-markets with both premium and upper-mid-range projects has helped it build considerable scale.

Other entrants with notable supply include Bengaluru-based Prestige Group and Sobha Ltd. Prestige accounts for 27% of these players’ overall NCR unit share, concentrated in Ghaziabad alone. Sobha’s 10% share is spread across Gurugram and Greater Noida. Shapoorji Pallonji, Birla Estates, Adani Realty, Tata Housing, and Mahindra Lifespaces have limited unit counts but have focused on high-value projects in strategic locations, particularly Gurugram.

Interestingly, most projects by these national players almost exclusively have large 3/4/5BHK configurations, with the average size 3BHKs clocking in at ~1,830 sq. ft., 4BHK at ~2,600 sq. ft., and 5 BHK at ~4,465 sq. ft.

“The limited supply of smaller configurations suggests that most national developers are targeting affluent, lifestyle-oriented homebuyers,” says Santhosh Kumar. “Average pricing across these developers’ projects falls within the premium category, with several of these developments positioned squarely in the luxury and ultra-luxury segments. Geographically, Gurugram remains their most preferred destination – of the total new supply in NCR by these national players, Gurugram has the highest share at 47%, followed by Ghaziabad with 27%, Noida 13%, and Greater Noida with 12%.”

Gurugram’s enduring appeal continues to be driven by strong corporate demand, superior infrastructure, proximity to the airport, and continued expansion of employment hubs.

The NCR Opportunity

NCR’s strong cross-border allure is fuelled by rapid urbanisation, rising demand for branded homes, and its constantly expanding corporate landscape. These dynamics accelerated post-COVID-19, as consolidation in the residential sector and NCR’s scale and connectivity made it an increasingly vibrant diversification market.

Major infrastructure projects – Dwarka Expressway, Noida International Airport, Delhi-Mumbai Expressway, RRTS, and metro expansions – are reshaping connectivity and unlocking new residential corridors with long-term potential.

“Residential demand from both end-users and investors is led by premium and luxury housing in Gurugram, Noida, Greater Noida, and New Gurugram. While end-user demand matches it in most precincts, investor activity is a prime demand driver in NCR,” says Santhosh Kumar. “Also, buyer preferences are shifting toward credibility and execution. Branded developers are gaining share, especially in the premium segments where buyers can depend on timely delivery, quality, and trust – mirroring trends seen in global real estate markets.”

Where does this leave regional developers?

“In securely familiar territory,” says Kumar. “The rise of national developers does impinge on regional players’ relevance, especially in their established location citadels. Local developers retain critical advantages, including deep market knowledge and entrenchment, strong land relationships and historic land banks, and established customer networks.”

Meanwhile, the growing presence of branded national players has elevated overall product quality, transparency, and customer confidence within NCR. They regularly introduce better design standards, larger amenity packages, sustainable construction practices, and stronger governance frameworks. Their entry has also intensified competition, encouraging local developers to improve execution capabilities and project delivery standards.

NCR remains one of India’s most vibrant growth markets. The luxury housing segment continues to outperform, and massive infra projects like Dwarka Expressway, Noida International Airport and regional transit networks create new development opportunities. As this market matures, its increasing share of organised and branded developers reinforces NCR’s position as one of the country’s most attractive residential real estate destinations.