Airport retail looks simple from the outside. You walk in, you browse, you buy. But the economics behind it are shaped by a few sharp forces, passenger mix, dwell time, and category behaviour that is very different from a typical high street. IRHPL’s latest internal read shows that international tourists contribute an estimated 35% to 45% of overall airport retail spending, making them the single most influential segment for value.

That share is not only about footfall. It is about basket value and category mix. International passengers disproportionately drive duty-free and luxury categories, which is why they “punch above their weight” in overall retail value.

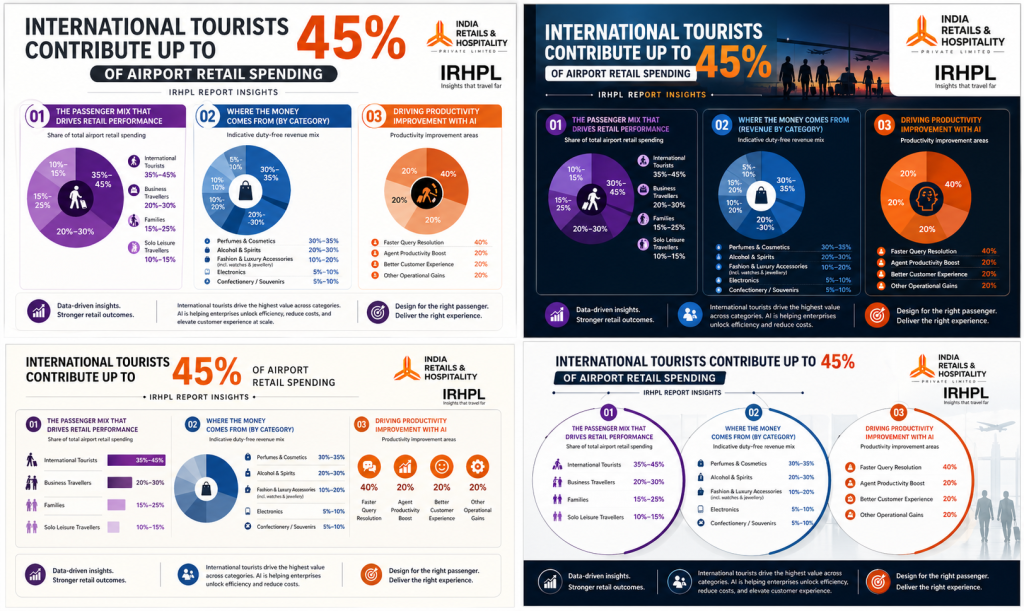

The passenger mix that drives retail performance

IRHPL’s segmentation breaks the market into four major traveller groups. Alongside international tourists at 35–45%, business travellers contribute 20–30%, families contribute 15–25%, and solo leisure travellers contribute 10–15% of retail spending.

Each segment behaves differently. International tourists are most likely to spend on duty-free and premium purchases. Business travellers are fewer in number but tend to have higher spend per trip, often leaning into lounges, quick F&B, convenience items and some duty-free. Families and leisure groups tend to drive everyday categories like food, essentials, and gifting.

Where the money comes from inside the terminal

Across airport stores, IRHPL highlights a typical global ranking of the highest revenue categories. Perfumes and cosmetics are often the single biggest category, contributing roughly 30% of duty-free or travel retail revenue, followed by alcohol and spirits at around 15–30%, with fashion and luxury accessories taking a growing double-digit share in premium hubs. Food and beverage is also called out as a large and growing share, alongside electronics, travel essentials, and confectionery or souvenirs.

This category mix explains why international tourists matter so much. These high-value categories are heavily influenced by duty-free shopping behaviour, gifting intent, and travel exclusives, areas where international travellers are most active.

IRHPL also shares an indicative duty-free revenue mix that helps explain the weight of the “big three” categories. Perfumes and cosmetics typically account for 30–35%, alcohol and spirits 20–30%, fashion and luxury accessories including watches and jewellery 10–20%, electronics 5–10%, and confectionery or souvenirs 5–10%.

F&B is driven by convenience, not dining

Food and beverage is often where airports see consistent daily demand, but it is not evenly split. IRHPL’s estimated global pattern suggests grab-and-go convenience formats account for 50–65% of F&B spend, while dine-in sit-down meals account for 25–35%, and premium beverages like specialty coffee, craft beer and bars account for 10–15%.

This split is important because it shapes what “winning” looks like in airport F&B. In many terminals, speed and predictability capture the majority share, while premium F&B becomes a yield play in higher-end hubs with stronger lounge penetration.

Luxury, essentials and gifting all coexist, but in different proportions

IRHPL’s estimates show that airport shopping is not only luxury-led. A typical spend-share breakdown suggests luxury goods and designer purchases can account for 20–35% of shopper spend, essentials like books, accessories and toiletries 25–35%, and gifting items like chocolates, regional sweets and souvenirs 20–30%.

This mix reinforces why airport retail needs balanced assortment planning. Luxury creates high-ticket value, essentials create consistency, and gifting creates impulse energy.

Impulse is real, but planned shopping dominates

A common assumption is that duty-free is mostly impulse. IRHPL’s data suggests the opposite balance. Impulse buys are estimated at 25–35%, while pre-planned purchases including pre-orders account for 65–75%.

This is a crucial planning insight. If most purchases are planned, then visibility and pre-order enablement matter more than many operators assume. At the same time, impulse still plays a major role, especially for giftable, portable categories. IRHPL lists the most common impulse categories as confectionery and small gifts, perfumes and cosmetics, and spirits or ready-to-drink travel exclusives.

Naresh Sharma, CEO, IRHPL Group of Companies speaks his mind saying, “Airport retail is not a footfall game anymore, it is a passenger-mix game. International travellers bring higher intent, higher basket value, and stronger premium conversion. The real opportunity for airports and operators is to design retail and F&B ecosystems around how these passengers actually spend, not around how many people walk past a storefront.”

Weekends, weekdays and the rhythm of sales

Sales patterns also shift based on the travel week. IRHPL notes that weekends typically show higher leisure footfall and stronger F&B and gifting, while weekdays (Mon–Thu) skew toward business traveller spend in lounges, quick F&B and some electronics or essentials. The magnitude can vary by airport type, but weekend sales can be around 10–25% higher in leisure-dominated airports, while business-centric hubs may see weekdays outperform.

Duty-free penetration and why international passengers matter

IRHPL also provides a useful planning range for duty-free purchase incidence. A typical range suggests around 30–60% of international passengers make at least one travel-retail purchase, depending on region, airport profile, traveller mix and local tax policy. For busy international hubs, IRHPL notes that modelling with 40–50% penetration is a reasonable baseline.

This reinforces the core headline. If international travellers are the group most likely to shop duty-free and spend in premium categories, their share of retail value will remain structurally high.

What IRHPL sees ahead

Looking forward, IRHPL forecasts travel and airport retail expansion at roughly 15–20% growth expectations over the next two to three years, driven by expansion across metros and airport concessions. On overall airport retail spending growth, IRHPL notes that recent market reports vary, but many point to mid-single to low-double digit YoY growth, around 6–12% depending on region and base effects.

When it comes to which traveller segment is growing fastest, IRHPL’s view is that leisure and international tourists are typically showing the highest growth in buyer numbers and purchase incidence, with business travel recovering steadily but often at a slower pace.

The takeaway for airport retail strategy

If international tourists contribute up to 45% of airport retail value, airports and operators need to design for that reality. IRHPL’s data makes one thing clear. Airport retail is no longer best understood as “shops in a terminal.” It is a passenger-behaviour business, and international tourists are currently its biggest value engine.