From Our Business Desk

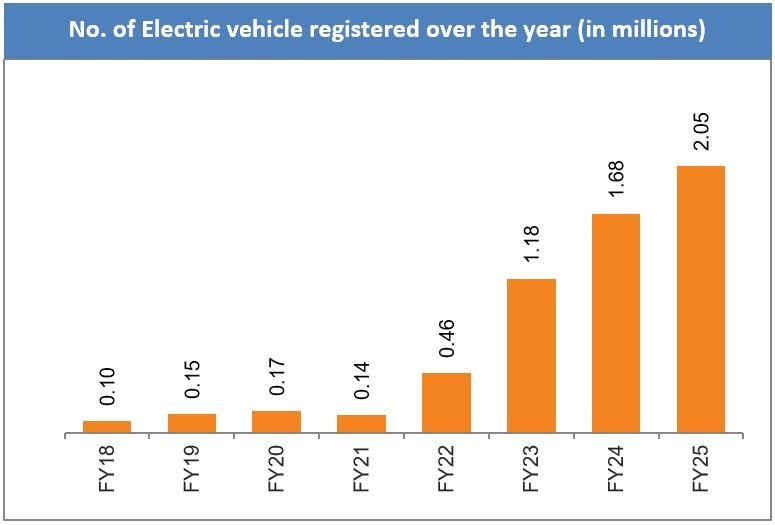

India’s electric passenger vehicle (PV) market witnessed robust growth in FY26 (April 2025–March 2026), with sales nearing or crossing the 2 lakh unit mark and overall penetration reaching around 4.2–4.9% of total passenger vehicle sales. Despite increasing competition from new entrants like Maruti Suzuki, VinFast, and others, the top three players—Tata Motors, JSW MG Motor India, and Mahindra & Mahindra—maintained overwhelming dominance, collectively securing approximately 87.3% of the EV market.

Market Overview and Growth Drivers

Electric car sales in FY26 grew significantly year-on-year (estimates range from 82–84% growth in some reports), driven by improving battery technology, expanding charging infrastructure, government incentives under schemes like FAME and PLI, falling battery costs, and a broader portfolio of affordable and premium EVs. Key models in the affordable and mid-range segments gained traction, especially in non-metro and Tier-2/3 cities.

Total EV passenger vehicle sales hovered around 2–2.29 lakh units, with the top three OEMs accounting for the lion’s share. Newer players collectively held only about 2% of the market, underscoring the established players’ strong brand trust, distribution networks, and product ecosystems.

Tata Motors: The Undisputed Leader

Tata Motors continued its reign as India’s EV king, selling roughly 78,000–92,000 electric passenger vehicles in FY26 (figures vary slightly across reports, with some citing ~77k–89k for core PV EVs). This translated to a market share of around 39–40.2%. While its dominance eased from over 50% in FY25 due to rising competition, Tata posted healthy volume growth of 35–43% YoY.

Key Contributors:

Nexon EV and Punch EV remained strong volume drivers.

Newer additions like the Harrier EV and Curvv EV helped expand the portfolio.

Tata achieved milestones such as cumulative EV sales surpassing significant thresholds, with strong quarterly performances (e.g., record highs in Q4).

Tata’s early-mover advantage, extensive service network, and focus on addressing adoption barriers (range anxiety, pricing, and warranties) solidified its position. Its EV penetration within its own PV sales was notably higher than the industry average.

JSW MG Motor India: Strong Second Place with Momentum

JSW MG Motor India (often referred to as MG Motor) delivered impressive growth, selling around 62,591 units of EVs in FY26—a 66% jump from FY25. This gave it a market share of approximately 26–27.3%.

Standout Performer: The MG Windsor EV emerged as a bestseller, particularly appealing in non-metro areas with its value proposition. Other models like the Comet EV and ZS EV contributed steadily, while newer launches (e.g., M9 MPV and Cyberster) added premium appeal.

MG’s strategy of aggressive pricing, feature-rich offerings, and rapid model refreshes helped it challenge Tata more effectively than in previous years.

Mahindra & Mahindra: The Fastest-Rising Challenger

Mahindra recorded explosive growth, with EV sales surging to around 42,000–54,000+ units (reports vary between ~42k–54k), achieving a market share of 21–23.9%—a massive leap from ~10.5% in FY25. In some segments and revenue terms, it even outperformed others at points during the year.

Key Models Driving Success:

XUV400, XUV 3XO EV, BE 6, XEV 9e, and XEV 9S.

The XEV 9S, in particular, became a top-seller in certain months.

Mahindra’s deep expertise in SUVs, combined with new electric platforms and a focus on the fast-growing SUV-EV segment, fueled its rise. It even briefly challenged for second spot on a monthly basis and led in revenue in some analyses due to higher average selling prices.

Competitive Landscape and Emerging Trends

New Entrants: Maruti Suzuki, VinFast, BYD, and others began making inroads but remained marginal (combined ~2–10% depending on exact data). Maruti showed multi-fold growth in select months, signaling future intensification of competition.

Monthly Highlights: In peak months like March and June 2026, Tata led with 8k–12k units, followed closely by Mahindra and MG in the 5k–7k range.

Challenges: Despite growth, overall EV penetration remained below 5% for passenger vehicles, hampered by infrastructure gaps, high upfront costs for some buyers, and policy uncertainties. Commercial EVs and two-wheelers saw parallel but distinct growth trajectories.

Outlook for FY27 and Beyond

The troika of Tata, MG, and Mahindra is well-positioned to drive India’s EV ambitions toward the 30% penetration target by 2030. Tata’s scale, MG’s agility, and Mahindra’s SUV prowess create a formidable core. However, intensifying competition, the need for localized battery production, and faster charging networks will be critical.

Expect more affordable models, battery-as-a-service options, and exports to play larger roles. Government support and industry investments (PLI schemes) should sustain momentum, though macroeconomic factors like fuel prices and consumer sentiment will influence the pace.

This FY26 performance marks a maturing Indian EV market—one where established domestic and joint-venture players continue to set the pace, laying a strong foundation for broader electrification in the years ahead. The “Big Three” have not just held the crown—they’ve strengthened their grip while the market expands.

*Data compiled from industry reports, Vahan portal insights, and company disclosures (approximate figures as reported across sources)