Gulf Conflict Tests India’s Resilience: Economic Costs of Geopolitical Balancing in a Volatile West Asia

By Suresh Unnithan

India is navigating a complex mix of economic pressures intensified by the escalating 2026 conflict in West Asia involving Iran, Israel, and the United States. The crisis, which worsened in late February with major disruptions to the Strait of Hormuz and ongoing ripple effects from earlier Red Sea shipping issues, has sent shockwaves through global energy markets, trade routes, and supply chains. Although India’s GDP growth held steady at approximately 7.4% in FY26 (with some estimates reaching 7.6% under revised series), the conflict has heightened risks of stagflation—persistent inflation alongside potential growth moderation—exposing vulnerabilities linked to the country’s foreign policy choices.

Critics suggest that the Modi government’s strengthened partnerships with Israel and the US—often described as “multi-alignment”—have complicated relations with Iran and added uncertainty to Gulf stability, threatening energy security, remittances, and export edges. At the same time, pragmatic moves like ramped-up Russian oil imports have offered important buffers, even as long-standing dependencies on West Asia endure. This analysis reviews the economic impacts with available data, the government’s countermeasures, and longer-term implications for India’s growth path.

Energy and Trade Disruptions: Geopolitical Shocks Hit Hard

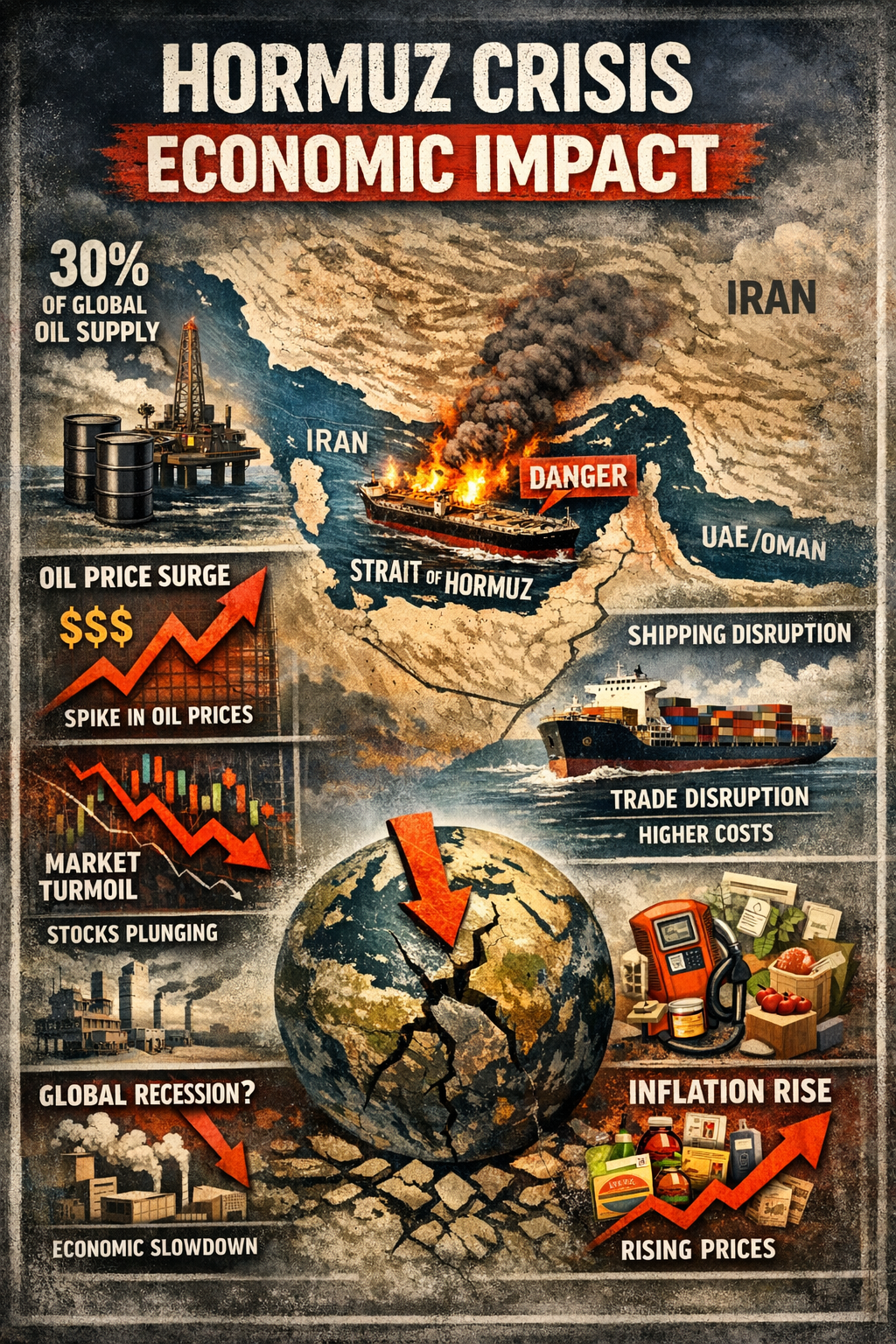

India relies on imports for about 85-88% of its crude oil, with West Asia traditionally accounting for a large portion—recently around 46-54% before the latest escalations, much of it passing through the Strait of Hormuz. The 2026 conflict forced rerouting via longer, more expensive paths like the Cape of Good Hope. Shipping costs jumped 15-20% in key corridors, echoing the strain from the 2023-2025 Houthi-related Red Sea disruptions. Global oil prices surged in March 2026, with India’s crude oil basket spiking dramatically—reaching peaks around $146-157 per barrel in mid-to-late March, more than doubling from pre-conflict levels near $69 in late February.

LNG and LPG supplies from the region also turned volatile, feeding into higher domestic fuel prices for CNG and LPG in several states, despite subsidies softening the blow for consumers. Exporters in tea, textiles, gems, and other sectors faced steep challenges: earlier Red Sea issues alone cut certain export categories by up to 9% by mid-2024, and 2026 extensions worsened delays and freight costs. Roughly 80% of India’s Europe-bound exports use these routes, squeezing margins for MSMEs and hurting competitiveness.

These events highlight India’s structural energy vulnerabilities. Russia has become the dominant supplier (its share surging to around 44% in March 2026 as Gulf volumes dropped sharply), followed by traditional players like Iraq, Saudi Arabia, and the UAE. Gulf dependencies persist, however, prompting renewed emphasis on boosting domestic production, building strategic reserves, and diversifying sources. ONGC and others have stressed long-term self-reliance measures.

India-Iran-Israel Dynamics: Partnerships Under Strain

India’s ties with Israel have delivered clear benefits in defense, technology, and innovation, though bilateral merchandise trade (excluding defense) declined from a peak of $10.77 billion in FY22-23 to around $3.6-3.75 billion in FY24-25 amid regional tensions. Defense cooperation has grown significantly, supported by high-level diplomatic engagements.

Relations with Iran, by contrast, have faced constraints from Western sanctions and India’s compliance needs. Bilateral trade remains modest at about $2.3 billion. The Chabahar Port project—key for bypassing Pakistan and enabling access to Central Asia via the International North-South Transport Corridor—continues but with challenges. India signed a 10-year operational contract in 2024, committing $370 million, and the port handled over 8 million tonnes of cargo by late 2024. US sanctions waivers (including a six-month extension into April 2026) and conflict uncertainties have slowed momentum and raised questions about sustained investment. India has signaled that exiting Chabahar is “not an option” and is engaging Washington to protect its interests.

Observers argue that a pronounced tilt toward Israel and the US has risked antagonizing Iran, potentially undermining Chabahar’s strategic value and future energy options. Yet Gulf partnerships—with the UAE and Saudi Arabia central to initiatives like I2U2—have stayed robust, supporting energy and economic ties. Remittances from the Gulf, forming roughly 38% of India’s total inflows (which hit a record $135-138 billion in FY25), remain a vital lifeline for millions of households, especially in states like Kerala. Escalation risks to migrant workers could dampen domestic consumption.

Inflation, Sectoral Pressures, and Currency Strain

Higher energy costs have pushed up inflation, particularly in the “electricity, gas, and other fuels” category in March 2026. Headline CPI stayed relatively contained at around 3.4% thanks to buffer stocks and interventions, but analysts flag risks of second-round effects if disruptions linger. Food inflation, already elevated in prior years, continues to weigh on rural areas where job creation lags headline growth figures.

Exporters grapple with elevated logistics costs that erode margins, while sectors like textiles and agriculture face delivery delays and buyer pushback on higher prices. The rupee depreciated sharply—by 9.5-9.88% in FY26, its steepest annual fall in over a decade—hitting record lows past 94-95 per USD. This reflects a stronger dollar, capital outflows, and import cost pressures from costlier oil. While depreciation can theoretically aid exporters, it amplifies imported inflation and debt burdens.

Government Response: Pragmatic Multi-Alignment

The government frames its approach as “multi-alignment”—building flexible relations across major powers rather than rigid alliances. In March 2026, PM Modi set up seven empowered inter-ministerial groups to oversee energy security, inflation, and supply chains, with short-, medium-, and long-term action plans. A proposed Economic Stabilisation Fund of about ₹573 billion (~$6.8 billion) targets support for affected sectors, including exporter relief schemes for freight costs. Defense links with Israel have strengthened, alongside diplomatic efforts to secure safe passage for Indian vessels and nationals.

Measures include accelerating crude source diversification, bolstering reserves, and forex interventions. Critics view this as leaning too heavily toward the US/Israel axis, potentially limiting leverage with Iran. However, continued Gulf engagement and Hormuz-related assurances demonstrate ongoing balancing. The conflict is testing the durability of this doctrine.

Growth Outlook: Strong Foundations, Emerging Risks

India began 2026 with solid fundamentals, including robust domestic demand and services exports driving 7.3-7.6% growth in early periods. Projections for FY27 range from 6.6-7.2%, with stagflation risks from energy volatility. Unemployment stands near 5.2%, and rural distress lingers amid food price pressures. Foreign exchange reserves offer a cushion, but prolonged shocks could widen the current account deficit. Remittances provide resilience, though Gulf instability introduces indirect risks.

Strategic Lessons: Toward Greater Autonomy

The 2026 West Asia crisis shows how foreign policy intersects with economic security. Closer Israel ties have brought defense and tech gains, but reduced Iran engagement and Hormuz exposure have raised costs through higher energy bills, rupee weakness, and export strains. A more neutral stance might have preserved greater flexibility with Tehran for Chabahar and oil diversification, yet US sanctions and security needs limit choices.

Diversification toward Russia and sustained Gulf partnerships have prevented worse outcomes, highlighting multi-alignment’s practical strengths. The episode underscores the importance of deeper strategic autonomy: speeding up renewable energy adoption, expanding domestic oil and gas production, and building resilient supply chains.

India’s growing economic weight gives it global influence, but this depends on ensuring foreign policy supports—not jeopardizes—domestic stability. The coming quarters will reveal whether current responses adequately protect 1.4 billion citizens from far-off conflicts or whether more decisive internal strengthening and recalibration are required. In an interconnected world, energy security and diplomatic agility remain central to sustaining India’s high-growth trajectory.

*Inputs from Nanditha Subhadra