By Suresh Unnithan

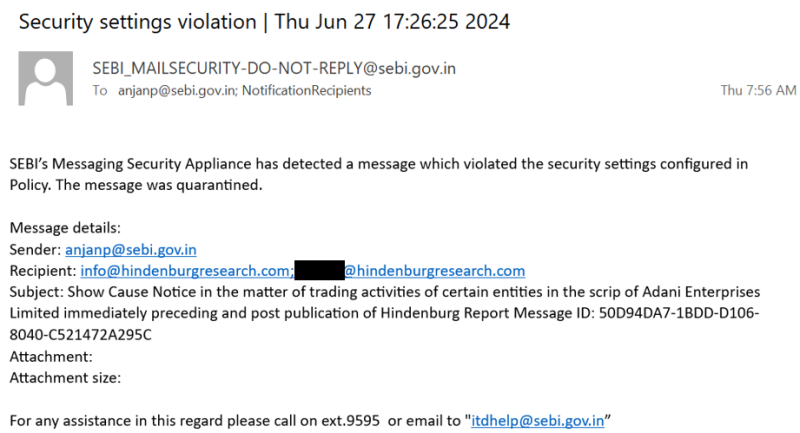

Thiruvananthapuram: Securities and Exchange Board of India (SEBI) has sent a show cause notice to the US-based short-seller Hindenburg Research seeking clarifications on its report on Indian business conglomerate Adani. The report published in August last year had accused Adani group of stock market manipulations. In an e-mail communication to this correspondent the short-seller has confirmed that it did receive a notice from the Indian stock market regulator, SEBI “on the morning of June 27, 2024.”

Hindenburg has described the notice as “nonsense, concocted to serve a pre-ordained purpose: an attempt to silence and intimidate those who expose corruption and fraud perpetrated by the most powerful individuals in India.” The short-seller in the e-mail has said, “Our original report was 106-pages, with 32,000 words, and included 720 citations, collectively detailing evidence that Adani engaged in a brazen stock manipulation and accounting fraud scheme over the course of decades.”

It has further said “following our initial Adani report, at least 40 independent media investigations corroborated or expounded on our findings, presenting evidence of widespread fraud by Adani against shareholders and Indian taxpayers, as detailed later.”

According to Hindeburg its report on Adani “provided evidence of a vast network of offshore shell entities controlled by Gautam Adani’s brother, Vinod Adani, and close associates. We detailed how billions were surreptitiously moved through these entities, into and out of Adani public and private entities, often without related-party disclosures. “

It has in the e-mail communication stated “we also detailed how a network of opaque offshore fund operators surreptitiously helped Adani evade minimum shareholder listing rules, citing numerous public documents and interviews to substantiate the allegations.”

Regarding the show cause notice Hindenburg says “the initial sections of SEBI’s 46-page Show Cause Notice to us outlined background on the Hindenburg report’s publication and an explanation of our relationship with an investor that expressed a short position in Adani.”

Explaining about the SEBI notice Hindenburg further said “much of the notice seemed designed to imply that our legal and disclosed investment stance was something secret or insidious, or to advance novel legal arguments claiming jurisdiction over us. Note that we are a U.S.-based research firm with zero Indian entities, employees, consultants or operations.”

According to the short-seller “some of these arguments seemed circular. For example, the regulator claimed that the disclaimers in our report were misleading because we were “indirectly participating in the Indian securities market,” and, therefore, were short Adani. This wasn’t a mystery—virtually everyone on earth knew we were short Adani because we prominently and repeatedly disclosed it. While SEBI seemingly tied itself in knots to claim jurisdiction over us, its notice conspicuously failed to name the party that has an actual tie to India.”

Hindenburg, in its e-mail, further said “shortly after our report, in August 2023, “Big-4” auditor Deloitte resigned from its role as statutory auditor for Adani Ports, citing undisclosed related-party transactions flagged in our report as the basis for a qualified opinion that accompanied its resignation. To this day, Adani has still failed to address the allegations in our report, instead providing a response that ignored every key issue we raised and has offered blanket denials.”

The short-seller says “after 1.5 Years Of Investigation, SEBI Identified Zero Factual Inaccuracies With Our Adani Research. Instead, The Regulator Took Issue With Things Like: Our Use Of The Word “Scandal” When Describing Multiple Prior Instances of Adani Promoters Being Charged With Fraud By Indian Regulators; And ii. Our Quoting Of An Individual That Alleged SEBI Is Corrupt And Works “Hand In Glove” With Conglomerates Like Adani To Help It Skirt Regulations.”

Explaining about its report on Adani, Hindenburg says, “Our report detailed how a Directorate of Revenue Intelligence (DRI) investigation found Adani had engaged in circular trading of diamonds, earning INR 6.8 billion (U.S. $151 million) in illicit export credits. We then described how CESTAT, the tribunal that handles appeals, dismissed the findings, effectively ignoring the earlier DRI conclusions.”

“SEBI did not allege any aspect of our description was false. Rather, it argued that CESTAT looked at the earlier case and alleged that we “sensationalized or distorted certain facts” by using the word “scandal” to describe the prior alleged INR 6.8 billion scheme by Adani that resulted in a 239-page order from the Commissioner of Customs detailing evidence of fraud, an INR 250 million (U.S. $4.6 million) fine, and extensive subsequent legal proceedings.”

Hindenburg in the e-mail says that its “report pointed out a 2007 SEBI ruling alleging that promoters of Adani worked with Ketan Parekh, perhaps India’s most notorious stock market manipulator, to manipulate shares in Adani. Our report explained how Adani Group entities initially received bans for their roles, but these were later reduced to token fines.”

According to Hindenburg “SEBI did not allege any aspect of this was false. Rather, SEBI claimed that it was a misrepresentation to call the reduction in punishment “leniency.”

“An apparently offended SEBI also claimed our report was not false, but rather “reckless” for quoting a banned broker with specific experience dealing with SEBI who detailed how the regulator was fully aware that firms like Adani used complex offshore entities to flout rules on minimum public shareholder ownership, and that the regulator participated in the schemes due to bribes. SEBI called the source “unreliable” as a banned broker.”

Concluding the narration Hinden stated that SEBI’s job as a “securities regulator is to detect and stop the types of malfeasance that we exposed. In our view, SEBI has neglected its responsibility, seemingly doing more to protect those perpetrating fraud than to protect the investors being victimized by it.”