From Our Business Desk

As India steps deeper into 2026, the official narrative from the ruling dispensation at the centre projects confidence and momentum. The government continues to highlight the country as the world’s fastest-growing major economy, pointing to strong GDP projections, expanding infrastructure, and a resilient services sector. Multilateral institutions have broadly supported this view, though with cautions regarding global headwinds.

The IMF raised its FY2025-26 (April 2025–March 2026) growth forecast to 7.3% in January 2026, citing strong momentum, before projecting a moderation to around 6.5% for calendar 2026 or FY2026-27. The World Bank in its April 2026 update raised India’s FY2026-27 growth forecast to 6.6% (from 6.3% earlier), while estimating 7.6% for FY2025-26, flagging risks from West Asia conflicts. The RBI has projected around 6.9% for FY2026-27, reflecting optimism on domestic demand but acknowledging external pressures.

Yet, beneath this optimistic projection lies a more complex and troubling reality. A closer examination of macroeconomic indicators from the Reserve Bank of India (RBI), Periodic Labour Force Survey (PLFS) by the Ministry of Statistics and Programme Implementation (MoSPI), National Statistical Office (NSO), IMF, World Bank, and rating agencies reveals structural weaknesses, external vulnerabilities, and deepening domestic stress that challenge the sustainability of this growth story.

The GDP Growth Paradox

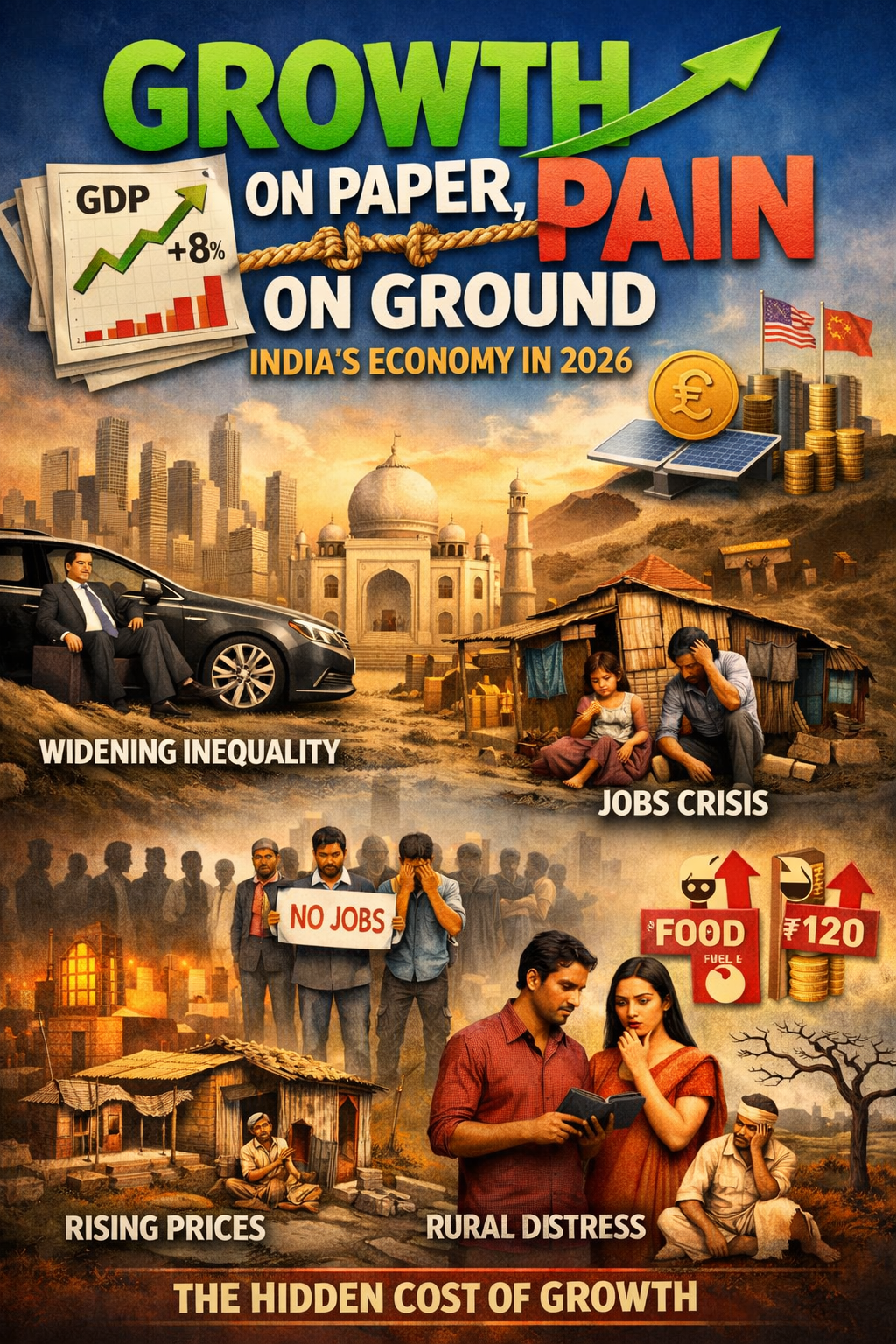

India’s GDP growth has been projected in the 6.5–7.6% range for FY2025–26 across sources. The NSO’s first advance estimates pointed to around 7.4%, with the IMF upgrading to 7.3% and the World Bank to 7.2–7.6% for the year. For FY2026-27, forecasts moderate to 6.5–6.6% (IMF/World Bank) or 6.9% (RBI).

However, the credibility of these headline figures faces scrutiny from economists. Discrepancies persist between high aggregate growth—driven by services (IT, finance, public administration) and government capital expenditure—and weaker ground-level indicators in private consumption, employment generation, and broad-based private investment. While the services sector shows robust expansion, agriculture and segments of manufacturing lag, leading critics to describe parts of the growth as “statistical” rather than fully substantive. Capacity underutilization in industry and cautious private sentiment further question the quality and durability of this expansion.

A Weakening Rupee and External Pressures

One of the most visible signs of strain is the persistent depreciation of the Indian rupee. In early 2026, the rupee touched record lows near ₹95.20 against the US dollar in March, with levels hovering around ₹93.80–94.30 in late April 2026, reflecting cumulative pressures and positioning it among Asia’s more vulnerable currencies amid global volatility.

This depreciation reflects deeper external vulnerabilities:

Rising Current Account Deficit (CAD): India’s heavy dependence on imported crude oil has widened the trade gap. The CAD stood at $13.2 billion (1.3% of GDP) in Q3 FY2025-26 (Oct–Dec 2025), up from $11.3 billion (1.1% of GDP) a year earlier, according to RBI data. The merchandise trade deficit expanded to $93.6 billion in that quarter. Cumulative Apr–Dec 2025 CAD was around $30.1–30.2 billion. Under sustained high oil prices due to West Asia tensions, the CAD risks widening toward 2% of GDP, per estimates from CRISIL and others.

FII Outflows and Capital Flows: 2025 and early 2026 saw episodes of substantial foreign institutional investor selling in equities and debt, signaling cautious global sentiment amid geopolitical risks and shifting US yields.

Trade Barriers: Protectionist measures and tariff pressures from partners like the United States have constrained merchandise export growth, even as services exports provide a partial buffer.

These factors intensify imported inflation risks and reduce macroeconomic stability, with the weaker rupee raising costs for external debt servicing and essential imports.

Debt: The Mounting Burden

India’s debt profile remains a key area of concern, as per RBI, IMF, and government data:

General Government Debt: Stood at approximately 81.9–83.4% of GDP in recent estimates (2024–2025 figures from RBI/IMF), elevated compared to pre-pandemic levels near 70%. Projections suggest it could trend around 78–80% in coming years, with the IMF placing it at 83.4% in its April 2026 outlook.

Central Government Debt: Targeted at 55.6% of GDP in Budget Estimates (BE) 2026-27, down slightly from 56.1% in Revised Estimates (RE) 2025-26. Total outstanding liabilities (internal + external) are projected to reach ₹214.82 lakh crore by end-March 2027.

External Debt: Rose to $765.5 billion by December 2025 (from $747.2 billion in September), with the external debt-to-GDP ratio relatively contained at around 19–20%, though short-term components add sensitivity to currency movements.

Household Debt: Climbed to 41.3% of GDP by end-March 2025 (RBI Financial Stability Report), up from a five-year average of ~38.3%, with some BIS-linked estimates showing around 45.5% in Q3 2025. This rise is driven by consumption-oriented retail loans and housing credit, with non-housing loans forming over 55% of household borrowings in recent periods. Per capita debt burdens have increased as households rely more on credit amid wage pressures.

While borrowing supports infrastructure and recovery, high debt servicing limits fiscal flexibility. The government targets gradual consolidation, with the fiscal deficit aimed at 4.3% of GDP in BE 2026-27 (from 4.4% in RE 2025-26), alongside a medium-term goal of reducing the central debt-to-GDP ratio toward 50% (±1%) by 2030-31.

Consumption Slowdown: The Silent Crisis

Consumption indicators present a mixed but concerning picture. Private final consumption has shown some resilience but faces underlying pressures from stagnant real wages in rural areas and urban cost burdens.

Rural Distress and Agriculture: Agriculture, employing over 40–45% of the workforce while contributing around 15–18% to GDP, has shown subdued growth. Recent estimates place agricultural GVA growth around 3.1–4.6% for FY2025-26 (with livestock and fisheries providing support, while crops remain volatile). Erratic monsoons, potential El Niño risks for 2026, rising input costs, and uneven price realization continue to strain rural incomes and demand for durables and FMCG.

Urban Strain: The middle class grapples with EMI burdens, high living costs, and job insecurity, tempering discretionary spending despite some urban recovery.

This uneven consumption dampens production cycles and overall momentum, with households increasingly relying on credit.

The K-Shaped Recovery: Growth for a Few

Post-pandemic recovery remains “K-shaped.” Large corporations in IT, finance, and select manufacturing report strong profits, while SMEs, informal sector workers, and rural populations lag. This duality widens inequality and limits the broad multiplier effects needed for sustained demand.

Unemployment and Jobless Growth

Employment generation remains a critical structural weakness. According to PLFS data:

Overall unemployment rate stood around 3.1% annually for 2025 (down from 3.2% in 2024), but monthly/quarterly readings under current weekly status show fluctuations, with figures around 5.0–5.1% in early 2026 (e.g., 5.1% in March 2026).

Youth Unemployment (15–29 years): Significantly elevated, with monthly readings around 14.7–15.2% in early 2026 and annual PLFS figures for 2025 showing ~9.9%. Educated graduates and urban youth face sharper challenges (graduate unemployment ~11.2%), reflecting skill mismatches.

Despite initiatives like “Make in India,” manufacturing and industry have not absorbed the growing labor force adequately, perpetuating underemployment in the informal sector and “jobless growth” concerns that threaten social stability and the demographic dividend.

Investment Hesitation and Capacity Underutilization

Private investment stays subdued. Industrial capacity utilization has hovered in the 74–76% range in recent quarters, below thresholds that typically spur fresh capex. Businesses remain cautious due to uncertain demand and global volatility. Growth relies heavily on public infrastructure spending, raising questions about the lack of a self-sustaining private investment cycle.

Fiscal Constraints and Policy Limitations

Fiscal space is tight. The government targets a 4.3% fiscal deficit for 2026-27 while prioritizing capital expenditure. High interest payments and potential subsidy pressures from food, fertilizers, and fuel (amid oil shocks) limit room for expanded welfare. This creates a policy dilemma between consolidation and supporting distressed segments.

Energy Shock and Inflation Risks

Geopolitical tensions in West Asia have pushed oil prices higher, increasing India’s import bill, transportation/production costs, and inflation risks (with IMF projecting CPI around 4.7% for 2026). Higher inflation could erode purchasing power further and widen the CAD, complicating RBI’s monetary policy. Sustained high oil prices could shave growth and strain subsidies.

Conclusion: A Fragile Equilibrium

India’s economic trajectory in 2026 reflects a fragile equilibrium. Headline GDP projections (ranging 6.5–7.6% for FY2025-26 and moderating thereafter across IMF, World Bank, RBI, and NSO estimates), infrastructure push, and services sector dynamism offer optimism and position India as a relative global outperformer.

However, weakening fundamentals—the rupee near historic lows (~₹94/USD), elevated general government debt (~82–83% of GDP), rising household leverage (41.3%+ of GDP), agriculture’s subdued growth (~3–4.6%), persistent youth unemployment (9.9–15.2%), sluggish private investment, and external vulnerabilities from energy shocks, trade imbalances, and a CAD of 1.3% in Q3 FY26—paint a more cautious outlook. Data from RBI, PLFS, IMF, World Bank, and NSO underscore the gap between statistical achievements and ground realities.

The central challenge is bridging this disconnect through structural reforms: enhancing employment generation, addressing skill mismatches, revitalizing rural economies and agriculture, reducing inequality, and crowding in private investment. Without inclusive and sustainable measures, the current model risks vulnerability to shocks. The narrative of resilience has merit in relative global terms and macroeconomic stability efforts, but it remains incomplete. For India to realize its long-term ambitions, policymakers must prioritize broad-based growth that translates into tangible gains in jobs, incomes, and living standards for the majority.